Last year, we presented backtested results for a VXX trading strategy. The system’s logic is based upon the concept of volatility risk premium. In short, the trading rules are as follows:

Buy (or Cover) VXX if 5D average of (VIX index -10D HV of SP500) < 0

Sell (or Short) VXX if 5D average of (VIX index -10D HV of SP500)>0

The strategy performed well in backtest. In this follow-up post, we look at how it has performed since last year. The Table below summarizes the results

| All trades | Long trades | Short trades | |

| Initial capital | 10000 | 10000 | 10000 |

| Ending capital | 3870.55 | 9095.02 | 4775.53 |

| Net Profit | -6129.45 | -904.98 | -5224.47 |

| Net Profit % | -61.29% | -9.05% | -52.24% |

| Exposure % | 100.00% | 14.67% | 85.33% |

| Net Risk Adjusted Return % | -61.29% | -61.68% | -61.23% |

| Annual Return % | -60.50% | -8.86% | -51.48% |

| Risk Adjusted Return % | -60.50% | -60.42% | -60.33% |

| All trades | 11 | 5 (45.45 %) | 6 (54.55 %) |

| Avg. Profit/Loss | -557.22 | -181 | -870.74 |

| Avg. Profit/Loss % | -3.35% | -4.40% | -2.47% |

| Avg. Bars Held | 24.55 | 8.6 | 37.83 |

| Winners | 6 (54.55 %) | 2 (18.18 %) | 4 (36.36 %) |

| Total Profit | 2366.97 | 365.38 | 2001.59 |

| Avg. Profit | 394.49 | 182.69 | 500.4 |

| Avg. Profit % | 13.75% | 6.46% | 17.40% |

| Avg. Bars Held | 32.5 | 7.5 | 45 |

| Max. Consecutive | 2 | 2 | 2 |

| Largest win | 1308.08 | 239.26 | 1308.08 |

| # bars in largest win | 102 | 8 | 102 |

| Losers | 5 (45.45 %) | 3 (27.27 %) | 2 (18.18 %) |

| Total Loss | -8496.42 | -1270.36 | -7226.06 |

| Avg. Loss | -1699.28 | -423.45 | -3613.03 |

| Avg. Loss % | -23.87% | -11.64% | -42.21% |

| Avg. Bars Held | 15 | 9.33 | 23.5 |

| Max. Consecutive | 2 | 2 | 1 |

| Largest loss | -6656.33 | -625.51 | -6656.33 |

| # bars in largest loss | 29 | 11 | 29 |

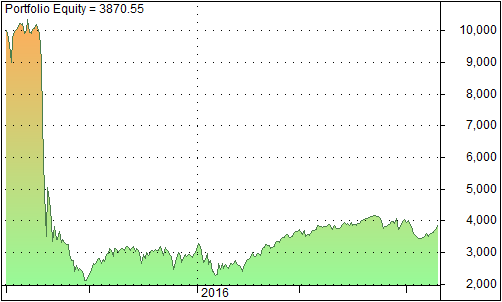

The strategy produced 11 trades with 6 trades (55%) being winners. However, it suffered a big loss during August. The graph below shows the portfolio equity since last August.

Large losses are typical of short volatility strategies. An interesting observation is that after the large drawdown, the strategy has recovered, as depicted by the upward trending equity line after August. This is usually the case for short volatility strategies.

Despite the big loss, the overall return (not shown) is still positive. This means that the strategy has a positive expectancy. Drawdown can be minimized by using a correct position size, stop losses, and a good portfolio allocation scheme. Another solution is to construct limited-loss positions using VXX options.