Last week the VIX index was more or less flat, the contango was favorable, and yet VIX ETF such as XIV, SVXY underperformed the market. In this post we will attempt to find an explanation.

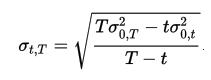

As briefly mentioned in the footnotes of the blog post entitled “A Volatility Term Structure Based Trading Strategy”, VIX futures represent the (risk neutral) expectation values of the forward implied volatilities and not the spot VIX. The forward volatility is calculated as follows,

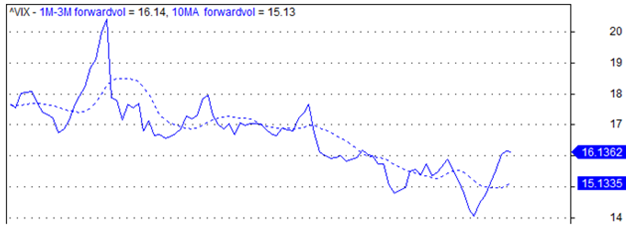

Using the above equation, and using the VIX index for σ0,t , VXV for σ0,T, we obtain the 1M-3M forward volatility as shown below.

Graph below shows the prices of VXX (green and red bars) and VIX April future (yellow line) for approximately the same period. Notice that their prices have increased since mid February, along with the forward volatility, while the spot VIX (not shown) has been more or less flat.

If you define the basis as VIX futures price-spot VIX, then you will observe that last week this basis widened despite the fact that time to maturity shortened.

In summary, VIX futures and ETF traders should pay attention to forward volatilities, in addition to the spot VIX. Forward and spot volatilities often move together, but they diverge from time to time. The divergence is a source of risk as well as opportunity.