It’s well known that there is a negative relationship between an equity’s price and its volatility. This can be explained by leverage or, alternatively, by volatility feedback effects. In this post, I’ll discuss practical applications to exploit this negative correlation between equity prices and their volatility.

A Trading Strategy Based on the Correlation Between the VIX and S&P500 Indices

This paper [1] examines the strong correlation in the S&P 500 and identifies trading opportunities when this correlation weakens or breaks down.

Findings

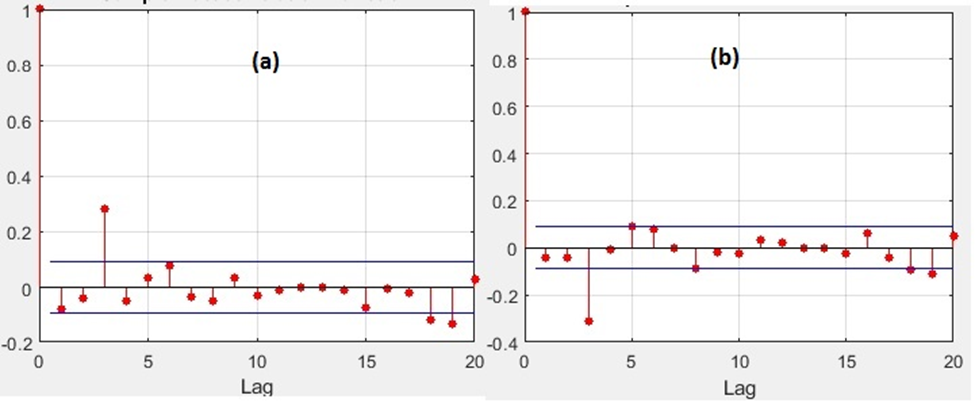

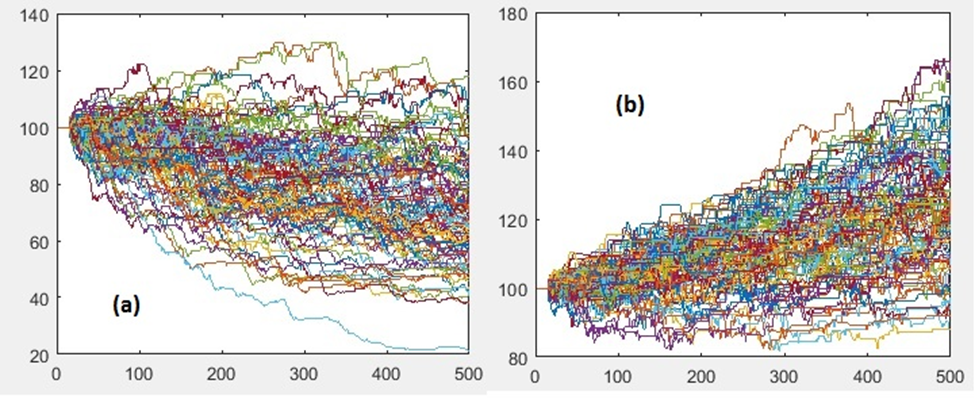

-The study covers the period from January 1995 to October 2020, utilizing 6,488 daily observations of the VIX and S&P500 indexes.

– In scenarios where the options market indicates increased drawdown risk with higher implied volatility but negative returns have not yet occurred, consider shorting the market.

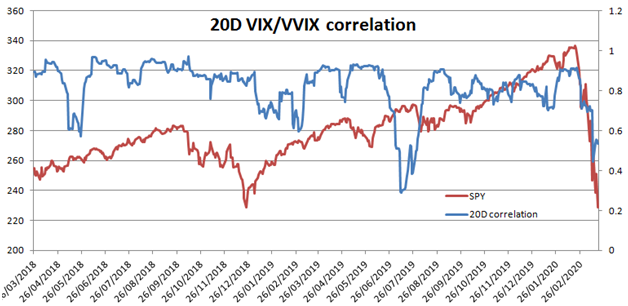

– The signal to short the market occurs when the negative correlation between the S&P 500 and VIX is broken, and they start exhibiting a positive correlation.

– The test setup involves identifying one or two consecutive days with positive co-movement between the VIX and S&P 500, then setting the transaction date for the day after or at the close of the chosen date.

– Empirical results show that the strategy outperforms the S&P500 index over the 25-year period, achieving higher returns, lower systematic risk, and reduced volatility.

-The findings provide evidence that excess returns can be generated by timing the market using historical data, even after accounting for trading costs.

Reference

[1] Tuomas Lehtinen, Statistical arbitrage strategy based on VIX-to-market based signal, Hanken School of Economics

Optimal Hedging for Options Using Minimum-Variance Delta

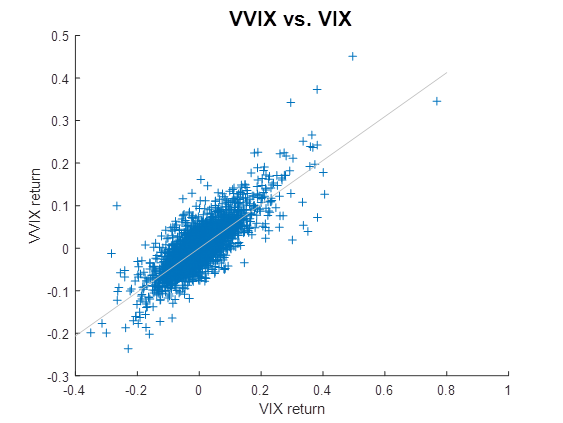

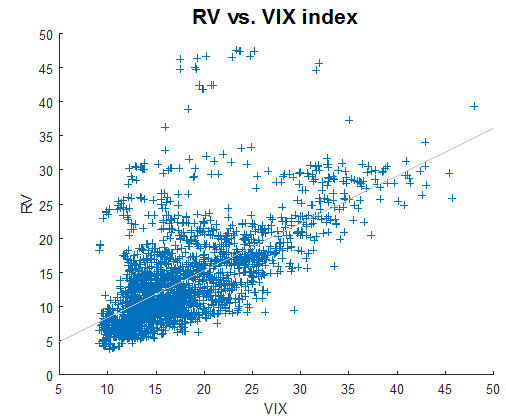

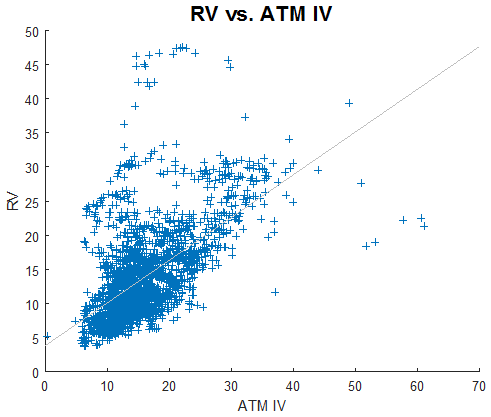

Contrary to the first paper, Reference [2] focuses on the strong correlation between the S&P 500 and its volatility, designing an efficient scheme for hedging an options book.

The authors developed a so-called minimum variance (MV) delta. Essentially, the MV delta is the Black-Scholes delta with an additional adjustment term.

Findings

-Due to the negative relationship between price and volatility for equities, the minimum variance delta is consistently less than the practitioner Black-Scholes delta.

-Traders should under-hedge equity call options and over-hedge equity put options compared to the practitioner Black-Scholes delta.

-The study demonstrates that the minimum variance delta can be accurately estimated using the practitioner Black-Scholes delta and the historical relationship between implied volatilities and asset prices.

-The expected movement in implied volatility for stock index options can be approximated as a quadratic function of the practitioner Black-Scholes delta divided by the square root of time.

-A formula for converting the practitioner Black-Scholes delta to the minimum variance delta is provided, yielding good out-of-sample results for both European and American call options on stock indices.

-For S&P 500 options, the model outperforms stochastic volatility models and models based on the slope of the volatility smile.

-The model works less well for certain ETFs

Reference:

[2] John Hull and Alan White, Optimal Delta Hedging for Options, Journal of Banking and Finance, Vol. 82, Sept 2017: 180-190

Closing Thoughts

These two papers take opposing approaches: one exploits correlation breakdown, while the other capitalizes on the correlation remaining strong. However, they are not mutually exclusive. Combining insights from both can lead to a more efficient trading or hedging strategy.

Educational Video

This seminar by Prof. J. Hull delves into the second paper discussed above.

Abstract

The “practitioner Black-Scholes delta” for hedging equity options is a delta calculated from the Black-Scholes-Merton model with the volatility parameter set equal to the implied volatility. As has been pointed out by a number of researchers, this delta does not minimize the variance of a trader’s position. This is because there is a negative correlation between equity price movements and implied volatility movements. The minimum variance delta takes account of both the impact of price changes and the impact of the expected change in implied volatility conditional on a price change. In this paper, we use ten years of data on options on stock indices and individual stocks to investigate the relationship between the Black-Scholes delta and the minimum variance delta. Our approach is different from earlier research in that it is empirically-based. It does not require a stochastic volatility model to be specified. Joint work with Allan White.